In the Guidelines for accounting for inventories (9), finished products are defined as part of inventories intended for sale, the technical and quality characteristics of which comply with the terms of the contract or the requirements of other documents in cases established by law.

Grade finished products. The following can be used as accounting prices for finished products:

- actual production cost (full and incomplete);

- standard cost (full and incomplete);

- negotiated prices;

- other types of prices.

Actual production costs are used mainly for single and small-scale production, as well as for the production of mass products of a small range.

It is advisable to use standard cost as accounting prices in industries with a mass and serial nature of production and with a large range of finished products. The advantages of these accounting prices are convenience in carrying out operational accounting of the movement of finished products, stability of accounting prices and unity of assessment in planning and accounting.

Negotiated prices are used mainly when such prices are stable.

When using standard costs, contractual and other types of prices as accounting prices, it is necessary at the end of the month to calculate the deviation of the actual production cost of products from their cost at accounting prices in order to distribute this deviation to the shipped (sold) products and their balances in warehouses. For this purpose, a special calculation is made (Table 9.1) using the weighted average percentage of deviations of the actual cost of products from their cost at accounting prices.

According to the table, this percentage turned out to be equal to 1 of the cost at discount prices.

Table 9.1

| N p/p | Indicators | At discounted prices | At actual cost | Deviation (+, -) |

|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 |

| 1 | Balance of finished goods at the beginning of the month | 300000 | 306000 | +6 000 |

| 2 | Received from production | 2 700000 | 2 724000 | +24 000 |

| 3 | Total | 3 000000 | 3 030000 | +30 000 |

| 4 | Ratio of deviations of the actual cost from the cost at fixed prices, % (gr. 5, p. 3: gr. 3, p. 3) | X | X | 1,0 |

| 5 | Finished products shipped | 2 500000 | 2 525000 | +25 000 |

| 6 | Balance of finished goods at the end of the month | 500000 | 505000 | +5 000 |

By multiplying the cost of shipped products and the cost of their balance in the warehouse at the end of the month by the calculated percentage, determine what part of the deviations is attributed to the products shipped and remaining in the warehouse (2,500,000 x 1: 100 = 25,000; 2,500,000 + 25,000 = 2,525 000).

500,000 x 1: 100 = 5000; 500,000 + 5000 = 505,000.

A similar calculation is made when using incomplete production costs. This calculation is not necessary if the organization uses account 40 “Output of products (works, services)” to record production output.

In practice, indicated in table. 9.1, calculations are made for homogeneous groups of goods (with approximately the same profitability), which ensures greater accuracy in calculating deviations.

Documentation of the movement of finished products

Receipt of finished products from production is documented with invoices, specifications, acceptance certificates and other primary documents.

Accounting for production at actual cost

Accounting for the availability and movement of finished products is carried out on active account 43 “Finished products”. This account is used by organizations in the material production industries. Finished products purchased for assembly or as goods for sale are recorded on account 41 "Goods". The cost of work performed and services provided to third parties is also not reflected in account 43 “Finished products”. The actual costs for them are written off from the production cost accounts to the debit of account 90 “Sales”. Products that are not subject to delivery on site and are not documented with an acceptance certificate remain as part of work in progress and are not taken into account in account 43 “Finished products”.

- in general for the work completed and delivered to the customer;

- for individual stages of work performed.

The first option is traditional, and accounting for the sale of products is carried out in accordance with one of the already described methods for accounting for the sale of products, works, and services.

In the second option, the calculation is carried out based on completed stages or complexes that have independent meaning, or the customer makes an advance to the organization until the work is completed in the amount of the contract price. In the second option, account 46 “Completed stages for work in progress” is used.

The debit of this account takes into account the cost of the stages of work completed by the organization, accepted in in the prescribed manner and reflected on the credit of account 90. At the same time, costs for completed and accepted stages of work are written off from the credit of account 20 to the debit of account 90. The amounts of received payment are reflected in the debit of cash accounts from the credit of account 62 “Settlements with buyers and customers”.

Upon completion of all stages of work, the cost of the stages paid by the customer is written off from account 46 to the debit of account 62 “Settlements with buyers and customers”. The cost of fully completed work recorded on account 62 is written off to the amount of advances received in the debit of account 62 “Settlements with buyers and customers” and to the amount received in the final settlement in the debit of cash accounting accounts.

If revenue from the sale of products, performance of work and provision of services cannot be determined, then it is taken into account in the amount of recognized expenses for the manufacture of these products, performance of this work and provision of this service (clause 14 of PBU 9/99). It follows from this that at least the following information is subject to disclosure as part of information about the organization’s accounting policies:

- on the procedure for recognizing the organization’s revenue (for individual stages of work or for all stages at once);

- on the method of determining the readiness of products, works, services.

Goods accounting

Concept and evaluation of goods. Goods are part of inventories acquired or received from other legal entities and individuals and intended for sale.

The procedure for assessing goods is determined by PBU 5/01 “Accounting for inventories”. In accordance with this PBU, goods are accepted for accounting at actual cost.

The actual cost of goods purchased for a fee is the amount of the organization's actual costs for the acquisition, excluding VAT and other refundable taxes; received under a gift agreement or free of charge - their market value; received under agreements providing for the fulfillment of obligations in non-monetary means - the value of assets transferred or to be transferred by the organization.

Organizations implementing trading activities, may include costs for the procurement and delivery of goods to central warehouses (bases), incurred until they are transferred for sale, as part of sales costs.

Organizations engaged in retail trade can evaluate purchased goods at their selling price with separate consideration of markups (discounts).

When goods are released for sale or otherwise disposed of (except for goods accounted for at sales value), they are assessed in one of the following ways: at unit cost; at average cost; at the cost of the first goods purchased (FIFO method).

Accounting for goods in organizations purchased for completing finished products and resale. To summarize information about the availability and movement of goods, synthetic account 41 “Goods” is used.

In organizations engaged in industrial and other production activities, account 41 “Goods” is used to account for materials, products, products purchased specifically for sale, or when the cost of finished products purchased for assembly is not included in the cost of products sold, but is reimbursed by the buyer separately .

Purchased goods and packaging are accepted for accounting under account 41 “Goods” at the cost of their acquisition. Goods accepted for accounting are reflected in the debit of account 41 and the credit of account 60 “Settlements with suppliers and contractors” and other accounts.

Receipt of goods can be reflected using account 15 “Procurement and acquisition of material assets” in a manner similar to accounting for corresponding operations with materials.

The accounting procedure for the sale of goods depends on the moment of recognition of revenue from the sale of goods.

When recognizing revenue from the sale of goods, the goods sold are written off to the debit of account 90 “Sales” from the credit of account 41 “Goods”.

If the proceeds from the sale of goods sold (shipped) cannot be recognized in accounting for a certain time, then until the revenue is recognized, the goods sold are recorded in account 45 “Goods shipped” (account 45 is debited and account 41 is credited). At the time of recognition of revenue from the sale of goods, their cost is written off from the credit of account 45 to the debit of account 90 “Sales”.

Finished products purchased for assembly and not included in the cost of products sold, when used, are written off from the credit of account 41, depending on the moment of recognition of revenue, to the debit of account 45 or 90.

At the time of revenue recognition, these finished products are written off from account 45 to account 90.

Analytical accounting of materials, products, products purchased specifically for sale, or the cost of finished products purchased for assembly and not included in the cost of products sold, is carried out in the manner prescribed for accounting for inventories.

Accounting for goods in wholesale and retail trade. Methods for evaluating goods. Organizations carrying out trading activities, on account 41 "Goods", in addition to inventory items purchased as goods for sale, also take into account purchased containers and containers of their own production (except for inventory, used for production or economic needs and accounted for on account 01 "Main means" or 10 "Materials").

The following subaccounts can be opened for account 41 “Goods”:

1 "Goods in warehouses";

2 "Goods in retail trade";

3 “Containers under the goods and empty”, etc.

Subaccount 1 “Goods in warehouses” takes into account the availability and movement of goods located at wholesale and distribution bases, warehouses, and storerooms of organizations providing services Catering, vegetable stores, refrigerators, etc.

Subaccount 2 “Goods in retail trade” takes into account the availability and movement of goods in organizations retail(shops, tents, stalls, kiosks, etc.), as well as in buffets of catering organizations. On the same sub-account, these organizations take into account the presence and movement of glassware(bottles, cans, etc.).

Subaccount 3 “Containers under goods and empty” takes into account the presence and movement of containers under goods and empty containers (except for glassware in retail trade organizations and buffets of public catering organizations).

Purchased goods and packaging are accepted by trade organizations for accounting under account 41 “Goods” at the cost of their acquisition. Goods accepted for accounting are reflected in the debit of account 41 and the credit of account 60 “Settlements with suppliers and contractors” and other accounts. Receipt of goods can be reflected using account 15 “Procurement and acquisition of material assets” in a manner similar to accounting for corresponding operations with materials.

In accordance with PBU 5/01, trade organizations can include costs for the procurement and delivery of goods to central warehouses (bases), incurred before the goods are transferred for sale, as part of sales costs.

Retail trade organizations are allowed to evaluate purchased goods at sales (retail) prices with separate consideration of markups (discounts). In this case, received goods are received at the cost of acquisition in the debit of account 41 and the credit of account 60 and other accounts. At the same time, account 41 is debited for the difference between the cost of purchasing goods and their cost at sales prices and account 42 “Trade margin” is credited.

The procedure for accounting for the sale of goods by trade organizations is carried out in the same way as in production organizations.

When recognizing revenue from the sale of goods upon their shipment (release), they are written off from the credit of account 41 to the debit of account 90 “Sales”.

If the proceeds from the sale of shipped (issued) goods cannot be recognized in accounting for a certain time, then the goods released are written off from the credit of account 41 to the debit of account 45 “Goods shipped”, and after recognizing the revenue - to the debit of account 90 from the credit of account 45.

Goods transferred for processing to other organizations are not written off from account 41. On account 41 they are counted separately.

Goods accepted for safekeeping and commission are recorded in off-balance sheet accounts 002 “Inventory assets accepted for safekeeping” and 004 “Goods accepted for commission.”

Analytical accounting for account 41 is carried out by responsible persons, names (grades, lots, bales), and, if necessary, by storage location of goods.

Features of using account 42 "trade margin"

Account 42 “Trade margin” is intended to summarize information about trade margins (discounts, markups) on goods in retail organizations that keep records at sales prices. This account also takes into account discounts provided by suppliers to retail organizations on possible losses goods, as well as for reimbursement of additional transportation costs.

Retail trade organizations that keep records of goods at sales prices usually receive goods received from suppliers as an accounting entry to the debit of account 41 “Goods” and the credit of account 60 “Settlements with suppliers and contractors” at purchase prices. To bring the purchase price of capitalized goods to the value at sales prices, the difference between the cost of purchasing the goods and their value at sales prices is determined and account 41 is debited for this difference and account 42 “Trade margin” is credited.

As goods are sold or disposed of for other reasons, the amount of the trade margin is written off from the credit of account 42 to the debit of accounts 90 “Sales” or 45 “Goods shipped” (for the sale of goods), 94 “Shortages and losses from damage to valuables” (for damage and shortage), 41 “Goods” (in case of natural loss) using the “red reversal” method.

The amounts of trade margins related to the goods remaining in the organization are clarified according to the inventory records by determining the applicable discount (mark-up) on goods in accordance with the established sizes.

The amount of a discount or mark-up on the balance of unsold goods can be determined based on the ratio of the amount of discounts or mark-ups on the balance of goods at the beginning of the month and the turnover on the credit of account 42 (excluding reversal entries) to the amount of goods sold for the month and the balance of goods at the end of the month (according to sales prices).

Analytical accounting for account 42 should ensure separate reflection of the amounts of discounts (mark-ups) and the difference in prices related to goods shipped and goods remaining in organizations.

Formation and accounting of reserves for reduction in the cost of goods

In accordance with paragraph 25 of PBU 5/01 (5), goods that are obsolete, have completely or partially lost their original quality, or the current market value of which has decreased are reflected in balance sheet at the end of the year minus the reserve for reduction in the value of goods.

A reserve for a decrease in the value of goods is formed at the expense of the financial results of the organization by the amount of the difference between the current market value and the actual cost of goods, if the latter is higher than the current market value.

The formation of a reserve for a decrease in the value of goods is reflected in the debit of account 91 “Other income and expenses” and the credit of account 14 “Reserves for a decrease in the value of material assets.”

At the beginning of the period following the period in which the above entry was made, the reserved amount is restored by an entry to the debit of account 14 and the credit of account 91 based on the assumption of complete consumption of goods in the next reporting period.

Accounting for sales expenses

Selling expenses include expenses associated with the sale of products (works, services) paid by the supplier. Selling expenses together with production costs form full cost products sold. Expenses associated with the sale of goods, works, and services are recorded in account 44 “Sales expenses.”

Selling expenses in organizations engaged in industrial and other production activities include:

- costs of containers and packaging of products in finished product warehouses (cost of services of its auxiliary workshops engaged in the manufacture of containers and packaging, cost of containers purchased externally, payment for packaging and packaging of products by third parties);

- expenses for transporting products (costs for delivering products to the station or pier of departure, loading into wagons, ships, cars, etc., payment for the services of specialized freight forwarding offices);

- commission fees and deductions paid to sales and intermediary organizations in accordance with contracts;

- advertising costs, including costs for advertisements in print and on television, prospectuses, catalogs, booklets, for participation in exhibitions, fairs, the cost of samples of goods transferred in accordance with contracts, agreements and other documents to buyers or intermediary organizations free of charge, and other similar expenses;

- other sales expenses (costs of storage, part-time work, sub-sorting, etc.).

In organizations that procure and process agricultural products (livestock, poultry, milk, wool, beets, etc.), account 44 “Sales expenses” may reflect general procurement expenses for the maintenance of procurement and receiving points, for the maintenance of livestock and poultry for bases and reception points.

In trade organizations, account 44 may reflect expenses (distribution costs) for the transportation of goods, wages, rent, maintenance of buildings, structures, premises and equipment, storage and processing of goods, advertising, entertainment expenses, and other expenses similar in purpose.

The Tax Code of the Russian Federation (Clause 4 of Article 264, Chapter 25) for tax purposes recognizes the following expenses as an organization's advertising expenses:

- for promotional events through funds mass media and telecommunication networks;

- illuminated and other outdoor advertising, including the production of advertising stands and billboards;

- participation in exhibitions, fairs, expositions, for the design of shop windows, sales exhibitions, sample rooms and showrooms, for the markdown of goods that have completely or partially lost their original qualities during exhibition. The specified advertising expenses are accepted for deduction when determining the tax base for income tax without restrictions, provided there are documents confirming these expenses.

Expenses for the purchase or production of prizes awarded to winners during mass advertising campaigns, as well as for other types of advertising, are accepted for tax purposes in an amount not exceeding 1% of revenue.

Choosing a method for accounting for output of products (works, services). In the Chart of Accounts accounting 2000, it is possible to record the output of products (works, services) in two ways: without using account 40 “Output of products (works, services)” and using this account.

The advantages and disadvantages of both options for accounting for output are discussed in Peculiarities of accounting for output when using account 40 “output of products (works, services)”.

Reserves for reducing the cost of finished products are formed in the same way as for inventories.

The main elements of the accounting policy for goods are:

- method of distribution of warehouse costs between types of material assets in non-trade organizations;

- method of distribution of costs for the sale of goods;

- method of analytical accounting of goods;

- the procedure for forming the purchase price of goods in trade organizations;

- a method for evaluating goods for retail organizations;

- method of evaluating goods sold;

- option for synthetic accounting of goods receipt;

- the procedure for forming reserves for reducing the cost of goods.

Methods for distributing warehouse costs between types of material assets in non-trading organizations. In accordance with paragraph 226 Guidelines according to inventory accounting in cases where in addition to goods, other material assets (finished products, materials, etc.) are stored in the organization’s warehouse, the costs of storing material assets are distributed between types of material assets in the following ways:

- proportional to their volume;

- proportional to their weight (mass);

- in proportion to their value.

The choice of a specific method for distributing warehouse costs between types of inventory depends mainly on their specific features.

Methods for allocating costs for the sale of goods. In accordance with clause 228 of the Methodological Guidelines for Accounting for Inventory, expenses for the sale of goods, as a rule, are written off in full on a monthly basis to the debit of the sales account (first option). If the amount of transportation and procurement costs associated with the acquisition (procurement) of goods and their delivery to the organization constitutes a significant share in the total revenue from sales of goods (more than 10%), then a proportional distribution of these costs is allowed between the actual cost of goods sold in a given month goods and their balances at the end of the month. In this case, the share attributable to the balances of goods not sold by the end of the month remains in account 44 “Sales expenses” and is transferred to the next month (second option).

Using the second option for allocating sales expenses allows you to more accurately calculate the cost of goods sold and unsold and can have a significant impact on profit indicators, book value of property and a number of other indicators.

The second option for distributing costs for the sale of goods is also recommended to be used if there is an uneven level of production of marketable products throughout the year (crop products, fisheries, etc.).

Methods of analytical accounting of goods. Analytical accounting of goods is carried out in physical value terms, i.e. by names of goods with their distinctive features (brand, article, grade, etc.) by quantity and actual cost.

In accordance with paragraph 240 of the Methodological Guidelines for Accounting for Inventory and Inventory, when maintaining natural value accounting, two methods can be used: different methods accounting of goods:

- varietal;

- party

When using the varietal method, goods are recorded on grading cards, reflecting the availability and movement of goods. The essence of the varietal method of accounting for goods is set out in paragraphs 136-140 of the Guidelines for accounting for inventories.

When using the batch method, accounting of goods is carried out not only by grade, but also for each batch of goods, which means goods received simultaneously under one document or under several documents. The batch accounting method should be used simultaneously in the accounting department and in the warehouse.

With the batch accounting method, analytical accounting of goods is carried out on special cards (batch cards), which are registered by assigning a number to each batch of goods. Each batch of goods is placed in a warehouse separately from other goods; the primary expenditure documents indicate the number of the batch card; turnover sheets for goods in the batch are compiled separately from other goods; After disposal of the corresponding batch, an inventory is taken for this batch of goods.

The batch method of accounting for goods is more labor-intensive compared to the grade method. At the same time, its use allows you to more effectively manage inventory.

The procedure for forming the purchase price of goods in the organization of trade. In accordance with clause 13 of PBU 5/01, organizations engaged in trading activities, costs for the procurement and delivery of goods to central warehouses (bases), incurred until they are transferred for sale, may include:

- in the cost of purchased goods;

- in selling expenses.

When assessing the consequences of decisions made on this element of the accounting policy, it is necessary to keep in mind that when using the first option, the cost of purchased goods turns out to be higher than when using the second option. In case of partial sale of goods, the balances of unsold goods are reflected in the corresponding balance sheet items in an overestimate, since the expenses for the sale of goods are fully or partially written off monthly to account 90 “Sales”, regardless of the fact of the sale of goods.

An increase in the cost of unsold goods overestimates the value of current assets and all property of the organization at the end of the month and affects all indicators calculated on their basis.

In addition, you need to take into account that in tax accounting fare are included in the cost of goods if provided for in the terms of the contract with the supplier. In other cases, transportation costs should be recorded as other expenses.

To simultaneously meet accounting and tax accounting It is advisable to take into account transport costs in the following accounts:

- 41 “Goods” - if they are included in the price of the goods under the terms of the contract;

- 44 "Sales expenses" - in other cases.

Methods for evaluating goods of a retail trade organization. Retail trade organizations can evaluate goods:

a) at sales price with separate consideration of markups (discounts);

b) at the cost of acquisition.

The choice of option for valuing goods is determined mainly by the possibility of using the natural-value method of accounting for the balances of the movement of goods (see Accounting for goods).

Methods for evaluating sold goods. When selling goods (except for goods accounted for at sales cost), they can be valued at the cost per unit of inventory, average cost, using the FIFO method (similar to materials).

The consequences of applying these methods for valuing goods sold are discussed in Elements of accounting policies for inventories.

Options for synthetic accounting of goods receipts. Synthetic accounting for the receipt of goods can be carried out using account 15 “Procurement and acquisition of material assets” or without using this account in a manner similar to the procedure for accounting for transactions with materials.

The procedure for forming reserves for reducing the cost of goods. Reserves for reducing the cost of goods are formed in the same way as for materials.

Disclosure of information about finished and shipped products, goods and sales expenses in financial statements

Information on the cost of finished and shipped products in the assessment provided for by the accounting policy (at full or incomplete, standard and actual cost) is contained in the second section of the balance sheet asset.

Goods are reflected in the balance sheet at a cost determined based on the methods used for valuing goods upon disposal (unit cost, average cost, FIFO method). An exception to this rule is goods accounted for at selling price.

Finished products and goods that are obsolete, have completely or partially lost their original quality, or the current market value of which has decreased, are reflected in the balance sheet minus a reserve for a decrease in the value of material assets.

At least the following information must be disclosed in the financial statements:

- on methods for evaluating finished, shipped products and goods;

- about the consequences of changing the methods of assessing finished, shipped products and goods;

- on the cost of finished, shipped products and goods pledged;

- on the amount and movement of reserves for reducing the value of these material assets.

Information on sales expenses for the reporting and previous years is contained in the income statement (form No. 2).

As part of the information on the organization's accounting policies in the financial statements, the procedure for recognizing sales expenses must be disclosed.

Exercise. Record invoice correspondence for transactions accounting for finished products and their shipment

| N p/p | Operations | Corresponding accounts | |

|---|---|---|---|

| debit | credit | ||

| Accounting for products at actual cost | |||

| 1 | Finished products were capitalized at accounting prices | ||

| 2 | Finished products intended for our own needs were transferred to the composition of materials | ||

| 3 | Finished products were returned to the workshop for refinement, etc. | ||

| 4 | The deviation of the actual cost of finished products from their cost at accounting prices was written off (by additional posting or the “red reversal” method) at the end of the month | ||

| 5 | Finished products were shipped on the basis of revenue recognition (at accounting prices) | ||

| 6 | Finished products were shipped, the sales revenue of which cannot be recognized in accounting for a certain time | ||

| 7 | The deviation of the actual cost of shipped products from its cost at accounting prices has been written off | ||

| Product accounting at discount prices | |||

| 8 | Finished products were capitalized at standard (planned) cost | ||

| 9 | Finished products were shipped at standard (planned cost) under the following conditions: revenue recognition; revenue cannot be recognized in accounting for a certain time | ||

| 10 | Actual production costs written off | ||

| 11 | The deviation of the actual cost of finished products from its standard (planned) cost has been written off | ||

| 12 | Costs for selling products are reflected | ||

| 13 | Expenses for selling products are written off | ||

| Transaction number | Sides of the account | |

|---|---|---|

| debit | credit | |

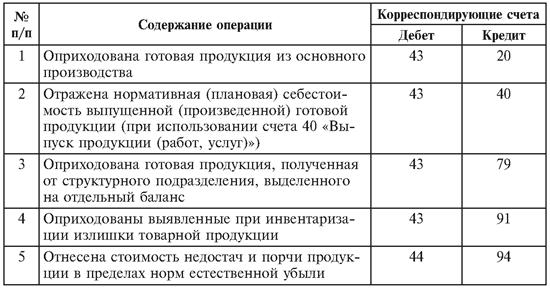

| 1 | 43 | 20, 23, 29 |

| 2 | 10 | 43 |

| 3 | 20, 23, 29 | 43 |

| 4 | 43 | 20, 23, 29 |

| 5 | 90 | 43 |

| 6 | 45 | 43 |

| 7 | 90, 45 | 43 |

| 8 | 43 | 40 |

| 9 | 90, 45 | 43, 43 |

| 10 | 40 | 20, 23, 29 |

| 11 | 90 | 40 |

| 12 | 44 | 10, 69, 70, etc. |

| 13 | 90 | 44 |

Finished products in the warehouse are recorded in warehouse accounting cards in kind or in qualitative and grade accounting books for similar material accounting.

With the balance method, the connection between the quantitative and grading accounting of products in the warehouse with their accounting in total terms in the accounting department is carried out using a statement of accounting for the balance of products in the warehouse. It is kept in the accounting department for a month. At the end of the month, the statement is transferred to the warehouse to reflect the balances of finished products in quantitative terms at the end of the month from the warehouse accounting cards (books) for each item number. After this, it is transferred to the accounting department, where the balances are taxed and their corresponding amounts are calculated.

Instead of a statement of product balances in the warehouse, the link between warehouse accounting and accounting can be a report from the financially responsible person on the movement of finished products in the warehouse for the month. It is compiled based on the final data of warehouse accounting cards (books), in which

the movement through the warehouse of finished products, each item number, is reflected in quantitative terms. In accounting, the report is taxed and, based on its data, a grading sheet is compiled. The movement of finished products, their shipment and sale in accounting is carried out in statement No. 16.

4. Documentation and accounting of shipment and sales of products

Shipped (dispensed) products, work performed and services provided mean products, works and services documented with relevant documents (invoices, acceptance certificates, etc.) for the shipment of finished products, delivery of works and services, as well as the transfer of products for sale.

Finished products (works, services), as a rule, are shipped to customers in accordance with supply contracts and the shipment plan. In accordance with the contracts, the sales department of the enterprise gives the finished product warehouse an order to ship the products to the buyer. All documents on shipped products, work performed and services provided are transferred to the accounting or financial department, where payment documents are issued in the name of the buyer. In particular, invoices, payment requests and payment requests for orders are drawn up here.

The accounting policy of the enterprise provides for a method of reflecting the sale of products at the time of shipment, upon presentation of payment documents to the buyer, or at the time of receipt Money for shipped products.

The moment of sale of goods is the moment at which goods shipped or released to the buyer are considered sold.

If the accounting policy of the enterprise reflects that the fact of sale is the moment of transfer to the buyer of products and settlement documents for the sale of products (works, services), then Product sales operations at the seller enterprise are reflected in the following accounting entries:

If the fact of the sale of products is considered to be the receipt of money into the bank account from the buyer, then to complete the sale transaction there must also be a fact of material transfer of the product to the buyer. Then for the seller company this product is considered sold. The following accounting records are compiled at the seller's enterprise:

Receipt of finished products from production is documented with invoices, specifications, acceptance certificates and other primary documents. But most often, invoices for the transfer of finished products to storage locations (Appendix 1). Documents reflecting the release and delivery of finished products have a general purpose, basically the same details, and are issued in two copies under the same number. They indicate the delivery workshop, the receiving warehouse, the name and item number of the product, the date of delivery, the discount price and the quantity of products delivered. One copy of the document is located in the production workshop, and the second in the warehouse. For each batch of products delivered, an entry is made in both copies of the acceptance documents. After completion of delivery of all products, in both copies of the acceptance documents for each name, type and grade, count and record the number of pieces or weight in numbers and words. Data

Invoices are signed by representatives of the delivery workshop, the recipient's warehouse and the technical control service.

An important condition for the correct organization of analytical accounting is, first of all, the good condition of the warehouse. Warehouses must meet product safety requirements, be insulated, equipped with security and fire alarms, and have weighing instruments. Products must be located in predetermined places, to which labels are attached indicating the name of the product, units of measurement, stock standards, actual availability, etc.

At the enterprise, agreements are concluded with financially responsible persons (warehouse managers, storekeepers) on financial liability, while the enterprise must create all conditions for the complete safety of material assets in the warehouse.

When organizing warehouse accounting of finished products, the order of their acquisition, packaging, transfer from production, storage and shipment plays an important role.

At many enterprises, finished products are assembled and packaged in production shops. They arrive at the warehouse in boxes that have a certain marking indicating the name of the finished product and its quantity. Using the same marking, without opening the boxes (boxes), the finished products are handed over to customers. At the same time, storekeepers do not check the contents of boxes (boxes) and are essentially responsible not for the quantity of accepted products, but for the number of accepted boxes (boxes) with products of a certain range. At such enterprises, it is necessary to keep records of the movement of finished products in the warehouse not only in physical and value terms, but also by the number of places (boxes) of a certain marking. Products received at the warehouse at most enterprises are stored in batches (stacks). A label is attached to each batch to control shelf life and the order of product release.

Warehouse accounting is maintained by financially responsible persons on product inventory cards. Form No. M-12 (Appendix 2).

They reflect the availability and movement of finished products in natural units of measurement (pieces, meters, kilograms, etc.). Cards are opened for each name (item number) of products in the accounting department and, against a signature in the registration journal, are transferred to the warehouse. The cards indicate the name, item number, grade, size and other characteristics of the product, registration price, storage location, and stock norm. For ease of operation, cards in the warehouse are placed in special box- a card index, where they are located by product groups, and within groups - by item numbers in ascending order. Cards of one group are separated from another by separators, on which the numbers and names of product groups are indicated.

Entries in cards are made by financially responsible persons on the basis of documents on the receipt of finished products into the warehouse and departure from the warehouse as operations are performed. At the end of the working day, the final balance is displayed in the cards where the movement of products was noted. At the end of the reporting period, the final balance is entered in all cards (regardless of whether there was or was no movement of finished products for a particular product name).

Cards can be filled out using technical means installed in the warehouse. Data on receipts and expenses are entered into warehouse accounting cards simultaneously with the issuance of primary documents. In addition, the warehouse maintains a book of receipts and disposals of products. Entries in cards are made on the basis of primary documents drawn up in the established order for the receipt and expenditure of material assets on the day of the transactions. After each entry, a new balance is displayed.

Accounting employees systematically check the correctness and timeliness of posting information from primary documents to warehouse accounting cards directly in warehouses in the presence of a storekeeper and confirm this with their signature.

All primary documents on the receipt and consumption of products from the warehouse are transferred to the accounting department. As a rule, such transfer is carried out directly at the warehouse. An accounting employee comes to the warehouse daily or once a week (ten days) and checks the correctness of the preparation of primary documents, entries in cards or the finished product accounting book for its receipt and consumption and the calculation of balances. Any errors found are corrected immediately. The accuracy of the calculated balances is confirmed in the cards or accounting book by the signature of an accounting employee.

After checking the entries in warehouse cards or the warehouse accounting book, the financially responsible person (warehouse manager, storekeeper) transfers the documents to the accounting employee. The transfer is formalized in a special register, filled out in two copies, the first of which remains in the warehouse, and the second, together with the documents, is transferred to the accounting department. At the end of the month, the warehouse manager (storekeeper) transmits information about products in natural units of measurement to the accounting department. The enterprise uses the balance sheet (operational accounting) method of accounting for material assets, then a balance sheet is filled out, into which balances from cards in natural units of measurement are transferred to the warehouse. In accounting, they are valued in monetary units.

IN Lately Many organizations use a cardless method of accounting for finished products. With this method, with the help of a computer, daily turnover sheets are compiled to record the release from production and the movement of finished products in relation to warehouses (other storage places). Finished product balances are periodically inventoried.

Accounting for the release of finished products. Accounting for the movement of finished products in storage and accounting areas

Finished products- these are products and semi-finished products that are fully processed and comply with current standards or approved technical specifications accepted by the warehouse or by the customer. It represents the end result production cycle economic activity organizations.

In accordance with PBU 5/01 “Accounting for inventories”, finished products are part of the organization’s inventories intended for sale, therefore, when accounting for finished products, General requirements requirements for inventory accounting. The finished products produced must, as a rule, be delivered to special finished product warehouses. These products are shipped externally, and some of them are constantly in the warehouse. Financially responsible persons are responsible for all its availability and movement. To ensure the reliability of accounting data on the availability of finished products, it is extremely important to carry out inventories, and for ongoing monitoring of their safety - inspections.

Necessary prerequisites for effective control over the safety of finished products are:

1. the presence of properly equipped warehouses and storerooms or specially adapted areas (for open storage stocks);

2. placement of product stocks in sections of warehouses, and within them in separate groups and type-varietal sizes (in stacks, racks, on shelves, etc.) in such a way as to ensure the possibility of their quick acceptance, release and checking of availability ; in places where each type of stock is stored, a label should be attached indicating information about the stock being held;

3. equipping storage areas for product stocks with weighing facilities, measuring instruments and measuring containers;

4. determination of the list of central (base) warehouses, warehouses (storerooms), which are independent accounting units;

5. determining the circle of persons responsible for the acceptance and release of product inventories (warehouse managers, storekeepers, forwarders, etc.), for the correct and timely execution of these operations, as well as for the safety of the inventories entrusted to them; concluding written agreements on financial liability with these persons in accordance with the established procedure; dismissal and relocation of financially responsible persons in agreement with the chief accountant of the organization;

6. determination of the list of officials who have the right to sign documents for the receipt and release of products from warehouses, as well as to issue permits (passes) for the removal of products from warehouses and other storage places.

Quantitative accounting of finished products by type and location of storage should be organized in two main ways : card and cardless . In the first method, grouping statements of receipt of products are compiled according to their types and storage locations. In the second method, daily turnover sheets are compiled (usually with the help of computers) to record the release from production and the movement of finished products to warehouses and other storage places.

Output from production with both the first and second methods is drawn up with delivery notes, specifications, acceptance certificates, etc.

The following primary documents are used to account for finished products:

1. delivery notes,

2. acts of acceptance and delivery of works (services),

3. railway receipts,

4. waybills,

5. payment requests-orders.

The release of finished products must be carried out under constant control by the organization’s accounting apparatus, since its uninterrupted receipt from the production process presupposes the timeliness of contractual relations with customers, the organization of settlements with the budget, off-budget funds, employees of the organization.

After the products have passed final stage production cycle, it is considered ready, and if it does not immediately go into sale, it is deposited with the financially responsible person (storekeeper).

Upon receipt of finished products, the financially responsible person, signing the document on the transfer of material assets (acts, invoices, etc.), leaves a second copy of it with himself. When products are removed from the warehouse, the accounting department prepares two copies of invoices, one of which is kept by the person who received the products, and the second remains in the warehouse. All movement of finished products should be reflected in warehouse accounting cards (form No. M-17) or, which is more convenient with a large range of goods and materials, in the warehouse accounting book (form No. M-40). These documents reflect the receipt, consumption and balance of each range of finished products.

At the end of the month, the financially responsible person draws up and submits to the accounting department a report on the movement of material assets, to which all the primary documents reflected in it are attached. Accounting for finished products by the financially responsible person is carried out, as a rule, in quantitative terms. The cost and total amounts are already indicated in the accounting department when processing material reports.

The actual movement of finished products in accounting is taken into account in production reports and reports on the movement of material assets, on the basis of which organizations draw up a statement of accounting for material assets, goods and containers. These statements are used in the future to fill out journal order No. 10/2.

After reconciling all the data reflected in primary documentation, with the information presented in the accounting registers, balance sheets are compiled in the accounting department.

Capitalization of finished products, based on their further use, can be made on account 10 “Materials” or on account 43 “Finished products”. “Materials” are credited to account 10 in the event that it is precisely known about its further use for the needs of the farm. In the event that the direction of use of the product is unknown, as well as when the finished product is sent for sale, it is reflected in the active balance sheet account 43 “Finished products”.

PBU 5/01 establishes the rules for the formation in accounting of information about the organization’s finished products. PBU 5/01 provides the following directions finished product assessments:

1) assessment of finished products upon receipt;

2) assessment of finished products when they are released into production or disposed of.

The main difficulty associated with accounting for finished products is due to the fact that when they are brought from the workshop to the warehouse, as a rule, no one knows and cannot know how much it cost to produce these products and, as a result, no one can say what their cost is. actual cost. For this reason, during the reporting period, these products are received and their movement is reflected at accounting (planned or other) prices, and only after the actual cost of the products has been calculated, the previously reflected in accounting assessment of the received and, accordingly, already shipped products is clarified - reported to actual. Finished products during the reporting period can be assessed using one of the following methods:

at actual production or reduced cost;

according to the planned (standard) production cost;

at wholesale selling prices;

at free selling prices and tariffs including VAT;

at free market prices.

Valuation based on actual production costs involves taking into account the sum of all costs for products. Reduced cost accounting excludes general business expenses.

This method is convenient to use in organizations with a limited range of serial products, when production and sales occur daily. The disadvantage of the method is the inaccuracy in determining production costs before the end of the reporting month.

When using the planned (standard) production cost to evaluate finished products, deviations of the actual production cost for the reporting period from the accounting price, ᴛ.ᴇ, are determined and separately taken into account. planned (standard) cost.

The advantage of this method is the unity of assessment in current accounting, planning and reporting. Moreover, if the planned cost changes several times during the year, then it is necessary to re-evaluate the finished product, which is very labor-intensive. If we take into account commodity output at the average annual planned cost, then accounting prices do not change during the year, but the cost of finished and sold products in the plan will not correspond to its cost indicated in monthly and quarterly reports.

When valuing at wholesale selling prices, the difference between the actual cost and the wholesale sales price is separately taken into account. The advantages of this method occur at relatively stable wholesale prices. It makes it possible to compare product assessments in current accounting and reporting, which is important for monitoring the correct determination of the volume of commodity output.

Valuation based on free selling prices and tariffs including VAT is used when performing single orders and work. With this assessment option, it is extremely important to separately take into account the amount of value added tax.

Finished products sold through the retail network are valued at free market prices.

When using all of the listed methods for assessing finished products, with the exception of assessment at actual production or reduced cost, it becomes extremely important to calculate deviations of commodity output in accounting prices from its actual cost. This allows, regardless of the valuation method in current accounting, to determine the actual cost of goods sold produced in a given month, as well as its balances in warehouses at the end of the month.

Accounting for the availability and movement of finished products is carried out, as noted above, on the active account 43 “Finished products”. This account is used by organizations in the material production industries.

On account 43, finished products can be accounted for both at actual production cost and at standard (planned) cost, which includes costs associated with the use of basic facilities, raw materials, materials, fuel, energy, labor resources and other production costs in the production process , or at direct costs.

On account 43 “Finished products” the following are not taken into account:

1. the cost of work performed and services provided to third parties (in fact, the costs for them are written off from the production cost accounts directly to account 90 “Sales”);

2. products that are subject to delivery to customers on site and are not formalized with an acceptance certificate (remains as part of work in progress);

3. finished products purchased for assembly (the cost of which is not included in the cost of the organization’s products) or as goods for sale (goods are accounted for in the organization in account 41 “Goods”).

The debit of the account reflects the receipt of finished products (from production, returns from customers, based on inventory results), and the credit reflects their write-off as a result of shipment, shortages, and return to production.

When accounting for finished products on account 43 at the actual production cost in analytical accounting, the movement of its individual items can be reflected at accounting prices (planned cost, selling prices, etc.) highlighting deviations of the actual production cost of products from their cost at accounting prices . Such deviations are taken into account for homogeneous groups of finished products, which are formed by the organization based on the level of deviations of the actual production cost from the cost at the accounting prices of individual products.

Accounting for the release of finished products. Accounting for the movement of finished products in storage and accounting areas - concept and types. Classification and features of the category "Accounting for the release of finished products. Accounting for the movement of finished products in storage and accounting areas" 2014, 2015.